文档主要内容

文档类型:学术论文

适用人群:审计专业学生、注册会计师、上市公司财务人员、企业内部控制管理者、证券监管机构从业者

文档核心内容:

该论文以登云股份为案例,系统分析上市公司关联方交易审计风险的形成机理、现状问题及防范对策。核心内容包括关联方交易审计风险的理论基础(舞弊三角理论、风险导向审计理论)、当前审计实践中存在的程序缺陷与人员素质不足、针对性的风险防范措施,以及登云股份关联方交易舞弊的具体案例剖析。

可解决的实际问题:

帮助审计从业者识别关联方交易中的舞弊信号,优化审计程序设计;为上市公司完善内部控制、降低审计失败风险提供参考;为监管机构加强行政惩处力度提供理论依据。

正文内容:

在全球经济一体化与行业竞争加剧的背景下,企业间的关联方交易日益频繁,但由此引发的审计失败案例也屡见不鲜。上市公司若要在发展中获取持续经济效益,必须基于行业趋势制定详细计划,并重点关注关联方交易中的审计风险。该论文以登云股份为具体案例,深入探讨关联方交易审计风险的理论框架、现实问题与应对策略。

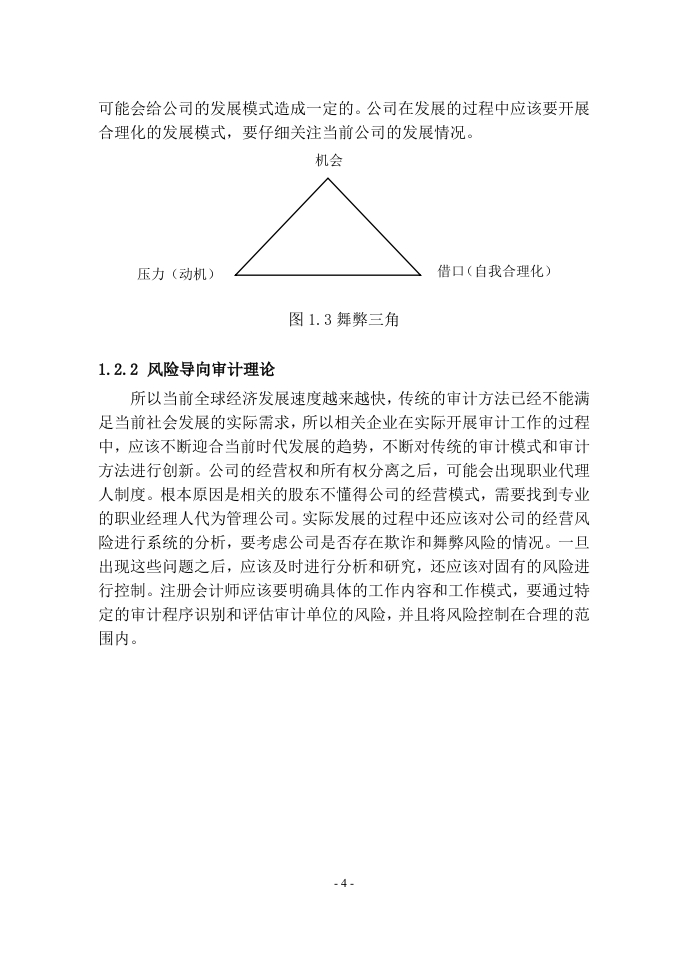

从理论层面看,关联方交易审计风险具有隐蔽性强、复杂性高的特点。论文引入舞弊三角理论,指出压力、机会与合理化借口是舞弊行为产生的三大要素;同时运用风险导向审计理论,强调审计工作应从企业整体风险出发,而非仅依赖传统程序。当前上市公司关联方交易审计存在两大突出问题:一是审计程序存在缺陷,未能针对特定关联交易设计有效测试;二是注册会计师职业技能与职业素质不足,难以识别复杂舞弊手段。

针对上述问题,论文提出三项核心防范对策。第一,为特定关联方交易建立有针对性的审计程序,例如强化对异常交易价格、交易频率及商业理由的核查。第二,提升审计人员执业水准,加强职业道德建设,确保其具备识别舞弊的专业敏感度。第三,加强行政监管并加大法律惩处力度,通过外部威慑降低舞弊动机。

在案例分析部分,论文聚焦登云股份。该公司在关联方交易中存在未披露的关联关系、异常资金往来等问题,导致审计风险显著上升。负责审计的信永中和会计师事务所未能有效识别这些风险,原因包括对关联方关系调查不充分、对异常交易信号忽视等。论文据此提出降低审计风险的具体措施,如扩大关联方核查范围、实施穿透式审计等。

结论与建议:

该研究通过理论分析与案例验证,揭示了关联方交易审计风险的核心成因与应对路径。关键结论包括:舞弊三角理论可有效解释关联方交易舞弊的动因;审计程序缺陷与人员素质不足是当前审计失败的主要根源;登云股份案例表明,忽视关联方关系核查是重大审计疏漏。建议审计机构在实务中强化风险导向思维,针对关联方交易设计专项程序,同时监管机构应提高违法成本,形成有效震慑。

文档评价:

该论文结构完整,从理论到案例层层递进,逻辑清晰。对登云股份的剖析具有典型性,提出的对策具备实操性,适合作为审计实务培训或学术研究的参考资料。

使用建议:

建议读者重点阅读第四章登云股份案例分析,结合舞弊三角理论理解审计失败的具体环节;审计从业人员可参考第三章对策部分,优化自身审计程序。

-177f7c9c1b-docx-1.webp)

暂无评论内容