文档主要内容

文档类型:学术论文

适用人群:会计从业人员、软件企业财务管理者、投资者、证券监管机构、高校财会专业师生

文档核心价值:本文以11家软件上市公司为样本,系统剖析研发费用核算与信息披露的六大痛点,并提出针对性改进建议,为优化企业财务报告质量、提升投资者决策有效性提供参考。

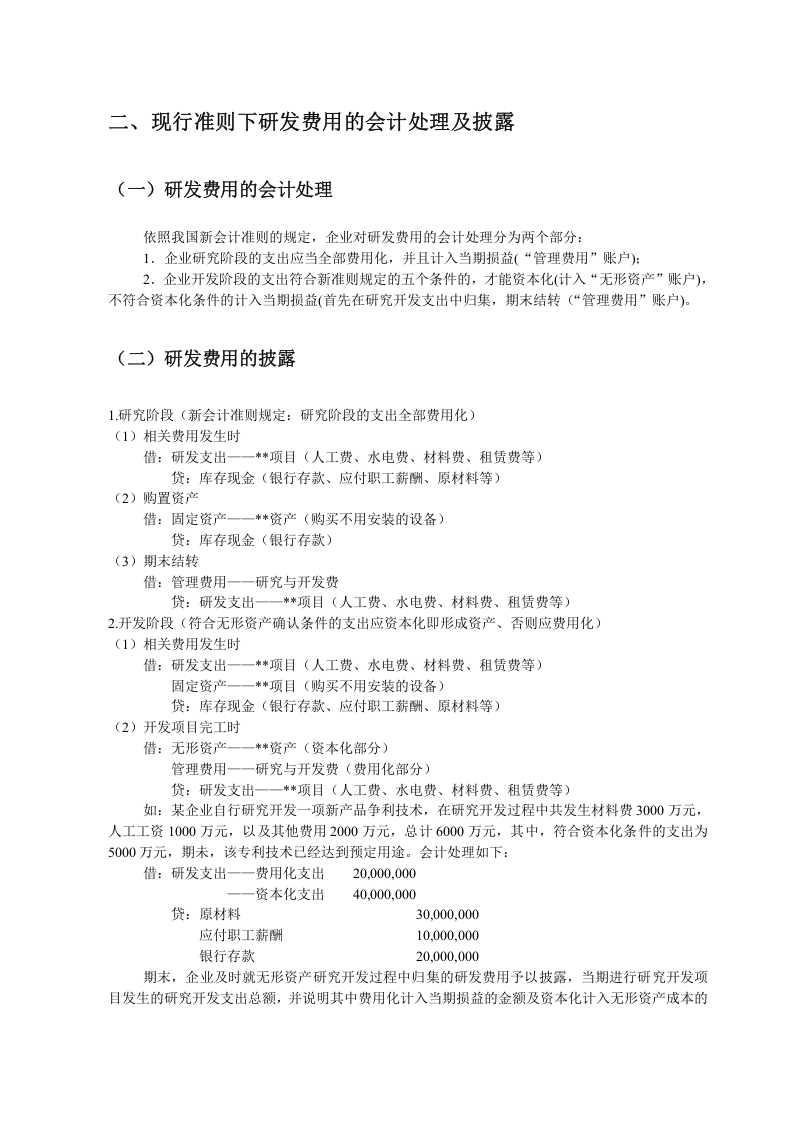

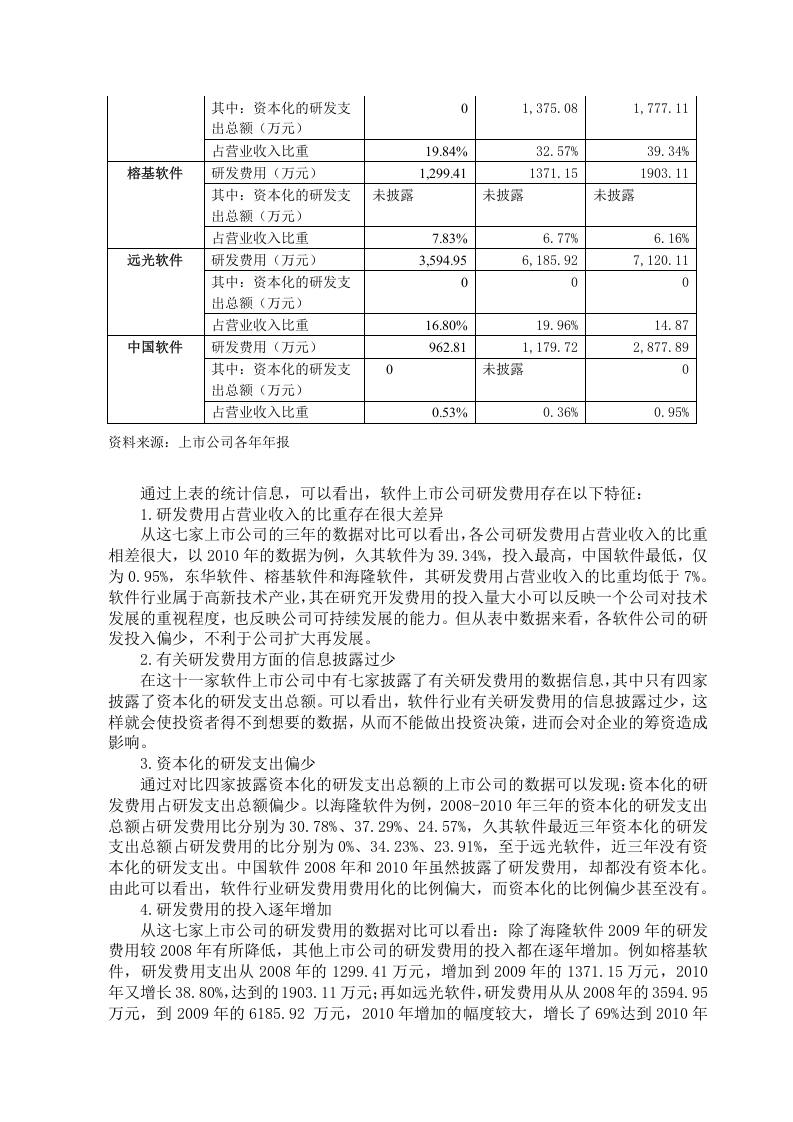

随着知识经济深化,研发能力成为软件企业竞争的关键筹码,研发投入占比持续攀升。研发费用的会计处理直接影响企业资产价值与利润表现,其信息披露质量也日益受到投资者关注。我国现行会计准则对研发费用采用有条件资本化处理,但规定存在诸多不足,导致核算难度增加。本文从无形资产、研发费用资本化与费用化等概念入手,梳理现行会计处理方法与原则,并以11家主营业务中软件业务占比最大的上市公司为研究对象,深入分析其研发费用信息披露现状。

研究发现,软件上市公司研发费用核算与披露存在六大突出问题:第一,开发阶段“资本化”五个条件的确认存在较大难度,主观性强,易被操纵;第二,计量单位单一,过度注重货币实物性,忽视技术价值、市场前景等非财务指标;第三,无形资产实际价值未得到充分反映,账面价值与真实价值偏离;第四,存在过度费用化现象,企业倾向于将研发支出全部计入当期损益,低估资产;第五,披露过于简单,形式散乱,缺乏统一模板,可比性差;第六,强制性披露制度安排不到位,企业自愿披露动力不足。

针对上述问题,本文提出以下建议:监管部门应进一步完善上市公司研发费用信息披露规范,制定具体实施规则,明确资本化条件的具体判断标准;鼓励企业采用多元计量方式,补充技术成熟度、市场预期等非财务信息;强化无形资产后续计量,定期评估其公允价值;规范披露格式,要求分阶段、分项目列示研发投入;加大强制性披露力度,对违规行为设定明确罚则。

核心结论:只有将研发信息披露落到实处,才能快速有效提高会计报告信息的相关性,满足信息使用者的需求。本文为软件行业研发费用核算的优化提供了实证依据与政策参考,对推动会计准则完善具有现实意义。

暂无评论内容