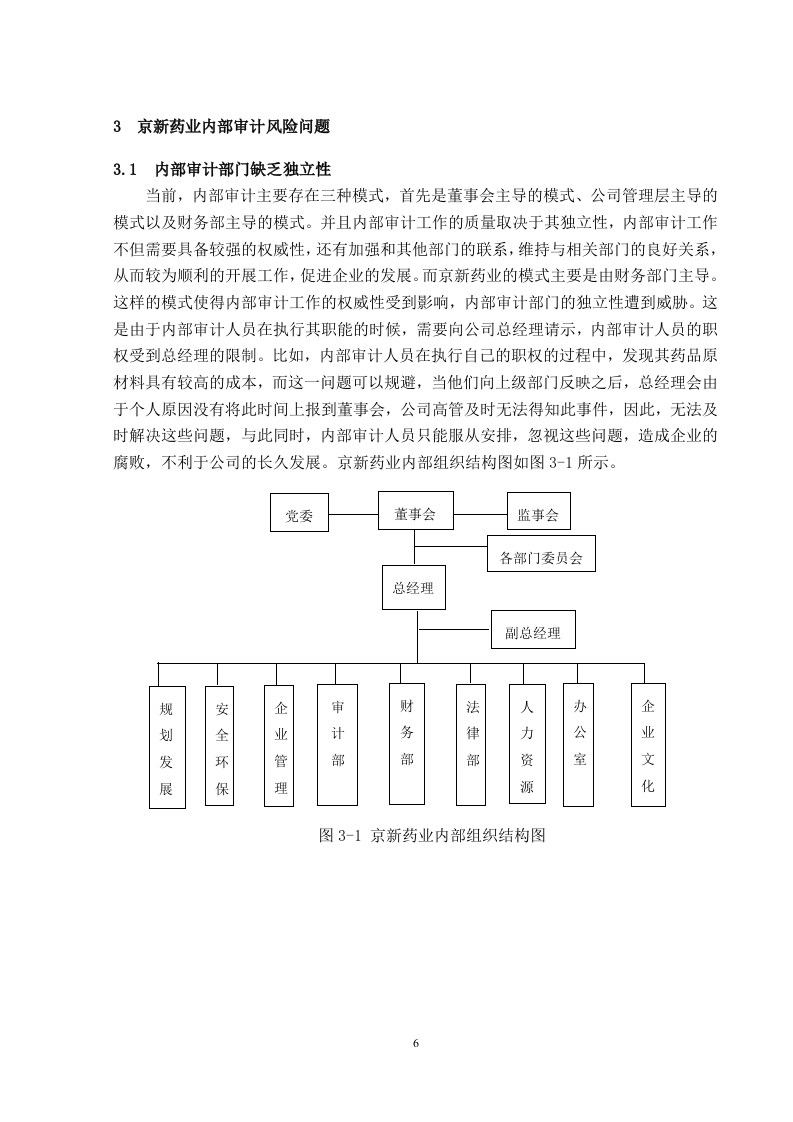

京新药业内部审计风险的规避及防范摘要:随着社会的进步,各大企业之间的竞争逐渐加剧,各个企业开始重视内部审计。内部审计对于公司和企业而言起着至关重要的作用,有利于企业和单位的发展,属于企业内部重点关注的监督内容。在当前阶段,企业之间的竞争加剧,对企业自身的发展有着更加重要的作用。因此,内部审计对于一个企业而言更加重要。尤其是企业内部的高层管理人员,需要注重发挥内部审计的积极作用,对企业发展提出新的目标和要求,使得整个企业在社会发展当中占据着优势的地位。本文主要以京新药业作为研究的对象,分析京新药业内部审计的现状,发现其存在的问题,并依据这些问题提出相应的对策和建议。同时,京新药业作为国家重点关注对象,其高新技术和制药科技在整个行业当中占据着重要地位,通过研究京新药业的内部企业,能够为相关人员提高一定价值的参考和借鉴。关键词:京新药业:内部审计风险:独立性Avoidance and Prevention of Internal Audit Risk of JingxinPharmaceuticalAbstract:Internal audit is an indispensable part of the development of an enterprise.It isthe content of important research and supervision within enterprises and units,and plays avital role in the development of enterprises.With the development of the economy and theadvancement of science and technology,the market competition is intensifying andcomplicated,the competition between enterprises is intensifying,and the market demands forenterprises are constantly improving.Therefore,enterprises need to give full play to thepositive role of internal audit work and escort the development of the company itself.JingxinPharmaceutical is a national key high-tech enterprise and one of the top 100 pharmaceuticalcompanies in China.The internal audit of enterprises also plays a vital role in thedevelopment of enterprises.In order to promote the development of Jingxin Pharmaceutical,this paper starts from the current internal audit status of Jingxin Pharmaceutical,and analyzesthe causes of the problems according to the status quo.Finally,it proposes the evasion andmethod measures for internal audit risks.It has played a positive role in promoting thedevelopment of Jingxin Pharmaceutical,thereby expanding the market competitiveness ofJingxin Pharmaceutical.Keywords:Jingxin Pharmaceutical;internal audit risk;avoidance and prevention录摘要.Abstract.............目录.............I绪…..21内部审计基本理论概述….31.1内部审计的含义和特征31.1.1内部审计含义.....31.1.2内部审计的特征..................3(3)审计程序的相对简化性3(4)审查范围的广泛性3(5)审计实施的及时性..1.2内部审计的职能.....……42京新药业简介和内部审计现状..….52.1京新药业简介......052.2京新药业内部审计现状分析..3京新药业内部审计风险问题....73.1内部审计部门缺乏独立性...73.2内部审计方法和程序有待改善.73.2.1内部审计方法落后..>3.2.2程序不规范......83.3内部审计范围不全面....4京新药业内部风险规避和方法对策..…94.1提高企业内部审计工作的独立性.94.2规范内部审计流程......104.2.1更新内部审计方法104.2.2强化后续审计..104.3拓宽内部审计范围..……….10结论......….11参考文献...12致谢.……….131目前,随着国家科学技术的进步,带动着整体社会的发展,我国的经济在大幅度的增长,各个行业的企业逐渐增加和兴起,使得这些企业之间的竞争加剧,对整体的竞争环境造成加大的压力。所以,针对这一现象,企业的内部审计不可忽视。近几年来,京新药业发展逐渐多元化,发展规模也在大幅的扩张,而企业内部的问题也开始暴漏出来。所以,内部审计部门作为京新药业的重要部分,对于京新药业的发展起着重要作用,尤其是面对不断变化的市场环境,寻找新的发展出路尤其重要。而通过内部审计,对公司内部审计风险进行探析,从而避免这些风险的产生,解决这些风险,提高审计的工作品质,一方面能够促进企业内部的发展规范化,另一方面,可以提高整个企业在行业内部的竞争能力。京新药业作为当前整个行业较为重要的制药企业,一方面,他的发展对整体行业有着重大的影响力,另一方面,它的发展方向必须符合当前的社会潮流,从而获取自己的独特竞争力。因此,京新药业需要立足于自己的自身,从内部寻找问题,针对问题的根源解决问题,对整个企业的内部审计的风险进行评估,管理企业内部审计部门,探究企业日常的各种经济来往和所发生的活动,对其进行管理和监督,提升企业内部的审计品质。所以,通过对京新药业的内部审计的分析和探究,排除其发展过程中的风险和问题,继而能够促进京新药业整体效益。在这篇文章中,以京新药业作为范例,首先概述内部审计的相关理论,对京新药业内部审计风险进行阐述,描写内部审计风险的含义和相关特点:其次,概述京新药业当前内部审计的状况,从内部审计部分框架和当前内部审计的三种模式,包括其存在的问题,仔细探究问题的根源,提出对应的解决策略,帮助京新企业规避风险,推动整个企业的发展和进步。在研究京新药业的内部审计部分的过程中,主要运用文献分析

-177f7c9c1b-docx-1.webp)

项目总承包管理组织方案-c9a0040014-docx-1.webp)

暂无评论内容