第1页 / 共27页

第2页 / 共27页

第3页 / 共27页

第4页 / 共27页

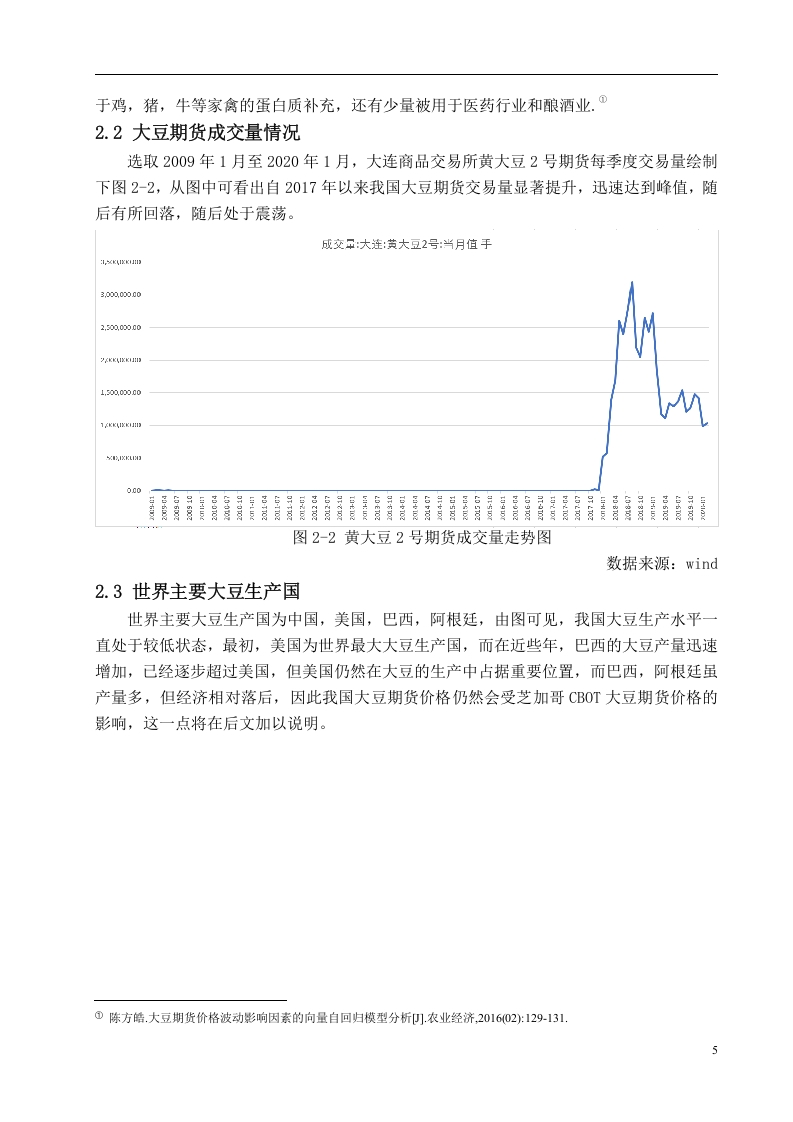

第5页 / 共27页

第6页 / 共27页

第7页 / 共27页

第8页 / 共27页

试读已结束,还剩19页,您可下载完整版后进行离线阅读

付费资源

© 版权声明

文章版权归作者所有,未经允许请勿转载。

THE END

基于VAR的中国大豆期货价格多因素建模研究是一篇学术论文,主要面向期货市场研究者、金融工程专业学生、农产品价格分析人员以及相关政策制定者。该文档系统梳理了大连商品交易所黄大豆2号期货价格的影响因素,并运用向量自回归模型进行实证分析,能够帮助读者理解期货价格波动的多因素驱动机制,为投资决策和风险管理提供量化参考。

研究背景方面,随着期货市场日益成熟,期货价格不仅为现货交易提供价格参考,也成为企业和投资者规避风险的重要工具。然而,期货价格频繁波动,探究其背后的影响因素及价格决策机制显得尤为关键。该论文选取中国期货市场中具有代表性的大连商品交易所黄大豆2号期货作为研究对象,从经济因素和市场因素两个维度出发,将供给冲击、需求冲击、大豆现货价格以及芝加哥CBOT大豆期货价格作为核心变量,构建了多因素向量自回归模型。

在实证分析过程中,论文使用Eviews10.0软件,首先对影响大豆期货价格的多个变量进行筛选与处理,最终确定五个关键变量。随后进行时间序列检验、ADF单位根检验以及格兰杰因果检验,在确认变量间因果关系后建立VAR模型。通过脉冲响应函数和方差分解,从线性表达和动态分析两个层面,研究各影响因素对大豆期货价格的作用路径与影响强度。脉冲响应函数揭示了某一因素发生冲击时,大豆期货价格在短期和长期内的响应轨迹;方差分解则量化了不同因素对价格波动的贡献程度。

研究结论表明,供给冲击、需求冲击、现货价格以及国际期货价格均对国内大豆期货价格产生显著影响,其中芝加哥CBOT大豆期货价格的传导效应尤为突出。该模型能够有效捕捉价格波动的动态特征,为期货市场参与者提供价格预测和风险对冲的参考依据。文档的独特价值在于将多因素纳入统一框架,通过严谨的计量方法验证了各因素的作用机制,适合用于学术研究、教学案例以及实际市场分析场景。

暂无评论内容