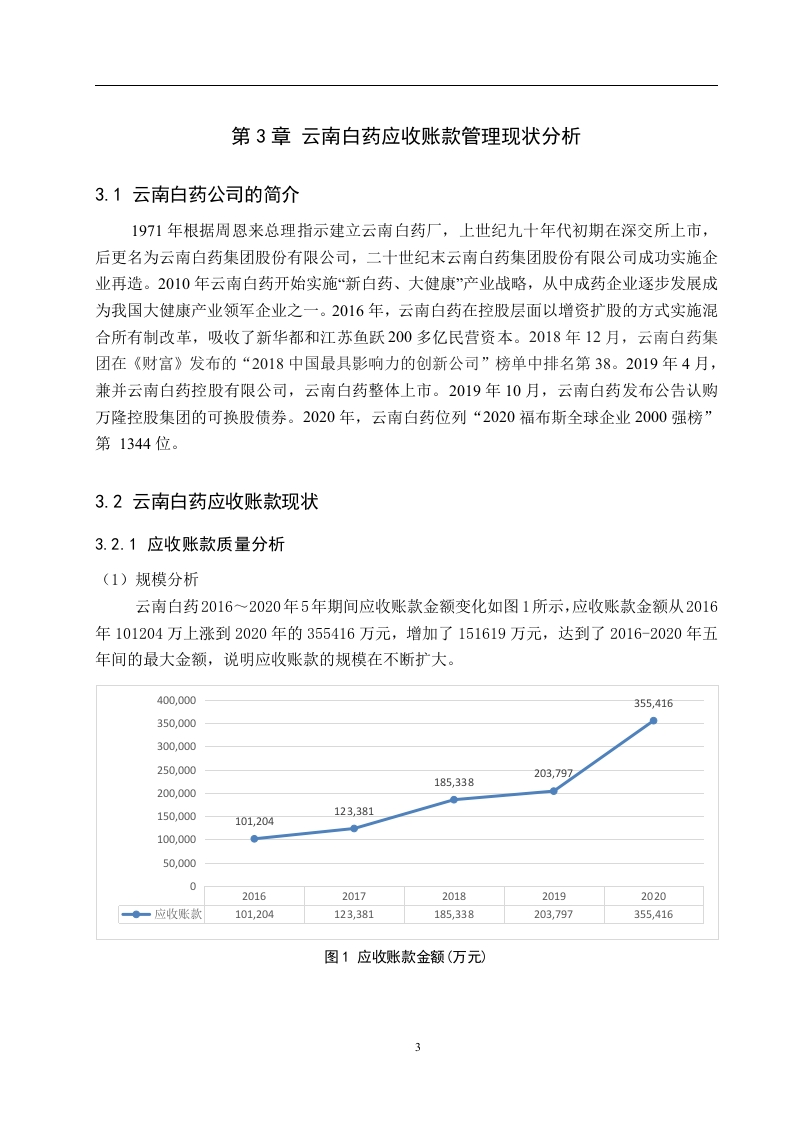

云南白药应收账款管理研究摘要应收账款管理是企业管理的重要环节之一。应收账款是企业促销的一种手段,能促进产品销量,提高企业销售额,增强企业核心竞争力,在一定程度上可以促进公司的利润增长。但是迫于竞争日益激烈的市场环境,许多企业放宽了销售条件,并扩大了赊销销售量,以便企业降低产品库存,更高的实现销售额,增加企业市场占有率。赊销增加了销售额的同时,也会导致应收帐款显著增加,这会严重阻碍业务运营和发展,影响企业资金周转,并造成不良坏账恶性循环。本文选用云南白药公司为研究案例,是因为在针对云南白药公司财务调查过程中发现其对于应收账款的管理有所欠缺。本文以企业应收账款管理为背景,针对目前云南白药公司应收账款的管理提出问题及分析原因,并为应收账款的问题提出解决方案。关键词:云南白药:应收账款:赊销1ABSTRACAccounts receivable management is one of the important links of enterprise management.Accounts receivable is a means of corporate promotion,which can promote product sales,increase corporate sales,enhance corporate core competitiveness,and to a certain extent canpromote the company's profit growth.However,due to the increasingly competitive marketenvironment,many companies have relaxed their sales conditions and expanded sales on credit,so that companies can reduce product inventory,achieve higher sales,and increase their marketshare.While credit sales increase sales,it will also lead to a significant increase in accountsreceivable,which will seriously hinder business operations and development,affect corporatecapital turnover,and create a vicious circle of bad debts.This article chooses Yunnan Baiyao Company as the research case because it is found that itlacks in the management of accounts receivable during the financial investigation of YunnanBaiyao Company.Based on the management of corporate accounts receivable,this article putsforward problems and analyzes the reasons for the current management of accounts receivable ofYunnan Baiyao Company,and proposes solutions to the problems of accounts receivable.Key words:Yunnan Baiyao;Accounts Receivable;Sales on Credit目录第1章引言...1.1研究背景1.2研究目的及意义....第2章应收账款相关理论概述..12.1应收账款的定义...2.2应收账款的影响......22.2.1应收账款的积极影响.22.2.2应收账款的消极影响..2第3章云南白药应收账款管理现状分析.33.1云南白药公司的简介.....33.2云南白药应收账款现状...33.2.1应收账款质量分析....。3.2.2应收账款政策分析...。。。。。。。6第4章云南白药应收账款管理存在的问题….64.1应收账款增速过快....4.2应收账款账龄长...…74.3应收账款回收速度减慢....7第5章云南白药产生应收账款问题的原因..·5.1企业盲目追求营业额....…5.2企业内部控制不健全,应收账款催收不利..……85.3各部门职责划分不够明确...。….85.4信用管理制度不完善第6章云南白药应收账款管理解决办法….96.1建立坏账准备金制度...·96.2加强内部控制,完善应收账款催收制度..96.3明确各个部门的职责,相互协作..….106.4完善应收账款信用管理制度.....……10...12参考文献...13致谢..…….14

项目总承包管理组织方案-c9a0040014-docx-1.webp)

暂无评论内容