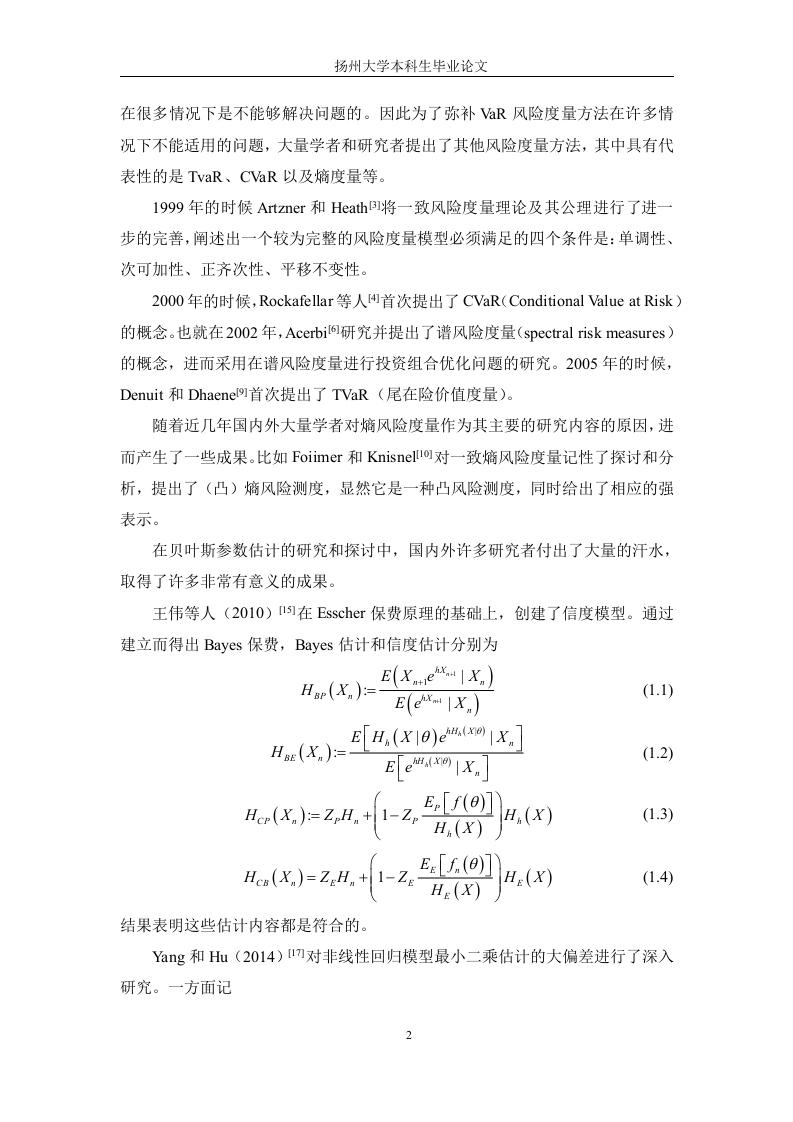

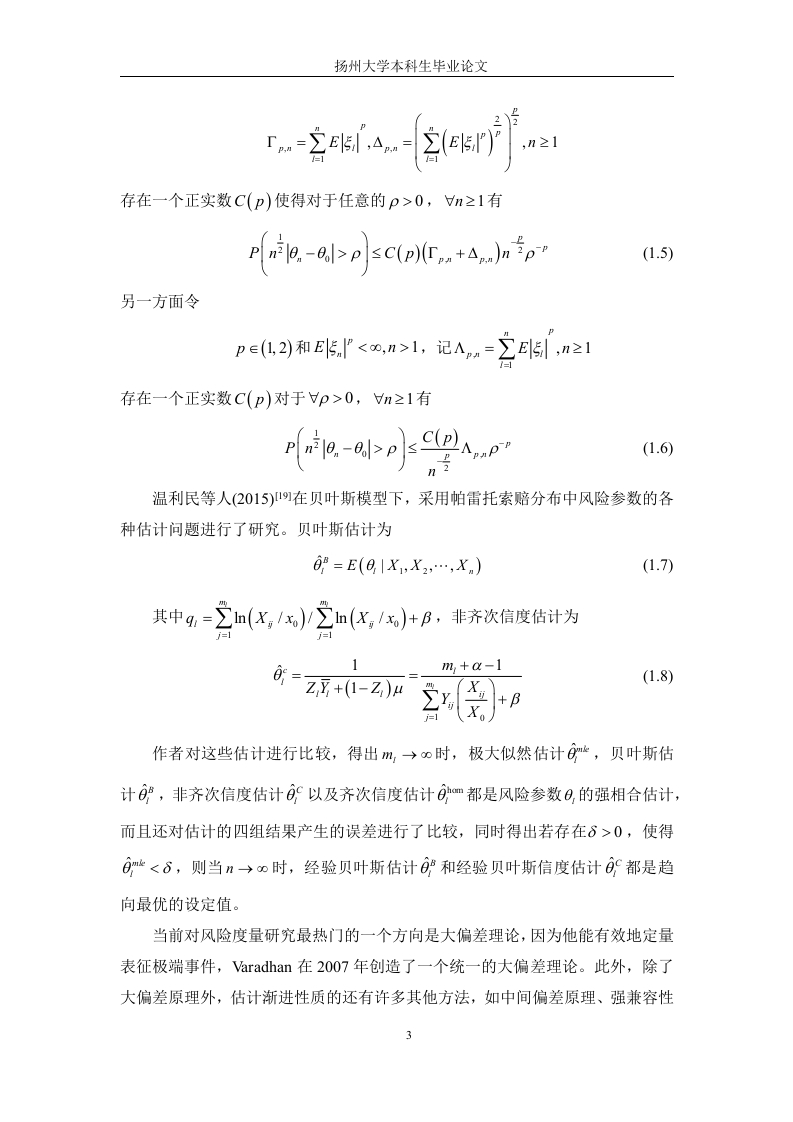

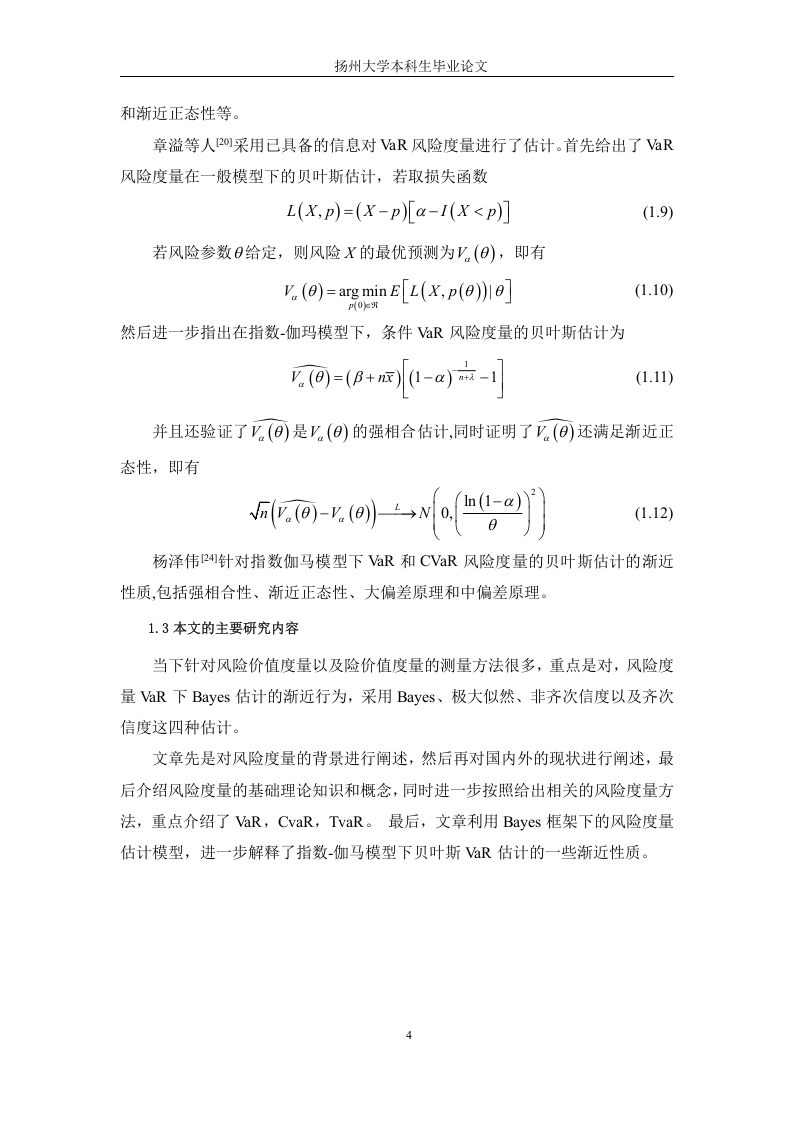

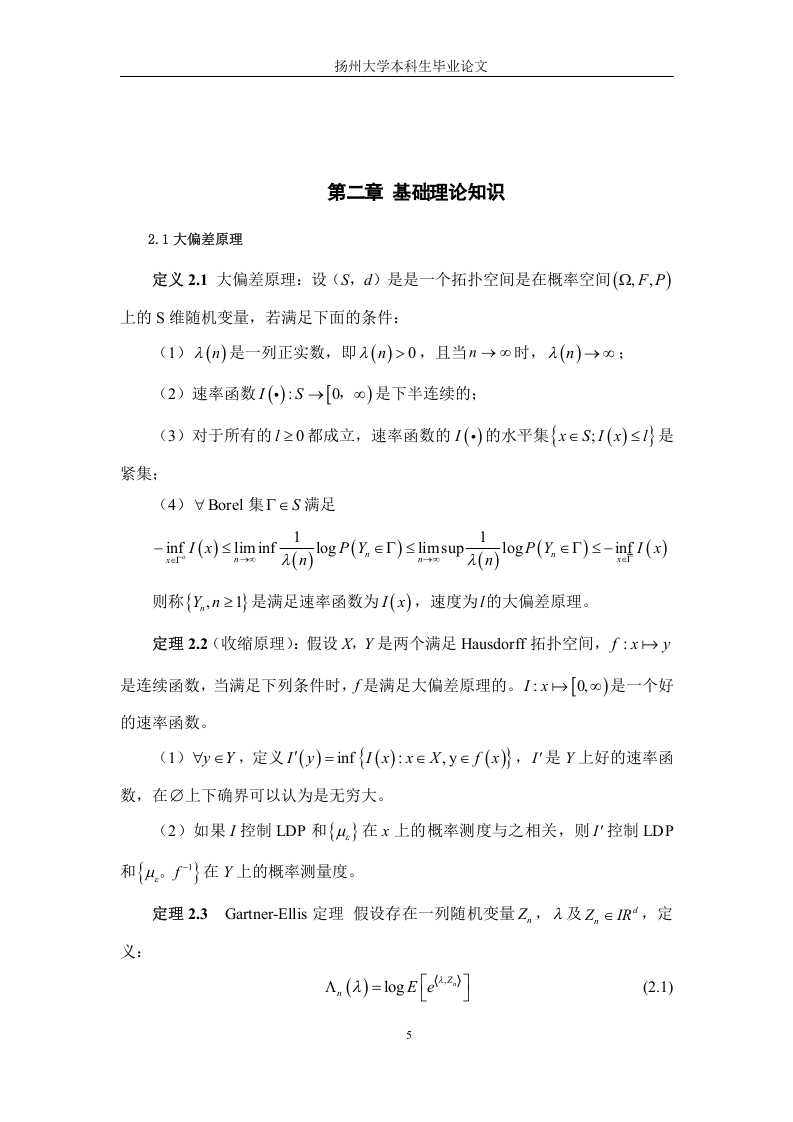

文档主要内容

随着全球经济一体化进程加速,金融风险受到国内外学者广泛关注。风险度量作为风险管理的关键环节,在当前经济全球化背景下具有重要研究价值。VaR(风险价值)的提出为风险管理做出了巨大贡献,但后续研究发现VaR在某些场景下存在局限性。

为弥补VaR的不足,学者们陆续提出CVaR、TVaR、熵风险度量等替代指标。风险本质上是不确定性问题,风险度量则是表达和分析这种不确定性的方式。风险随机变量的分布与特定风险参数之间存在依赖关系,因此需要对这些参数进行估计并解释其极限性质。

当前可用的估计方法包括极大似然估计、非齐次可靠性估计、齐次可靠性估计以及贝叶斯估计。贝叶斯估计具有多种极限性质,如大偏差原理、强互换性、渐近正态性以及中偏差原理。通过分析VaR风险度量的贝叶斯估计的渐近行为,并结合指数-伽马模型给出的贝叶斯估计,可以验证该估计满足大偏差原理和相容性。

文档类型:论文。适用人群:金融风险管理研究人员、统计学家、量化分析师、金融工程专业学生。可解决的实际问题:帮助读者理解VaR贝叶斯估计在极限条件下的统计行为,验证其理论性质,为风险度量方法的选择提供理论依据,同时为后续研究其他风险度量的渐近性质提供参考框架。

该论文的核心贡献在于:通过指数-伽马模型具体验证了贝叶斯估计的渐近行为,确认其同时满足大偏差原理和相容性。这一结论表明,在特定模型设定下,贝叶斯估计能够有效处理风险参数的不确定性,并具有稳健的极限性质。对于从事风险度量理论研究的学者而言,该结果可作为进一步推导其他模型下贝叶斯估计渐近性质的基准。对于实际应用者,理解这些性质有助于判断在何种条件下贝叶斯估计优于其他估计方法。

总之,该论文系统梳理了VaR贝叶斯估计的渐近行为,结合指数-伽马模型给出了理论验证,为风险度量领域的理论研究和实际应用提供了重要支撑。

暂无评论内容