主要内容

预览文档 文档类型:论文

适用人群:油脂油料加工企业管理者、期货市场投资者、金融研究人员、高校经济类专业师生

文档核心内容:

该论文以2018年1月6日至2023年3月25日的国内棕榈油期货价格与现货价格周数据为样本,运用VAR模型、协整检验、格兰杰因果检验、脉冲响应分析和方差分解等实证方法,系统研究了中国棕榈油期货市场与现货市场之间的价格联动关系。研究证实,国内棕榈油期现货价格存在长期均衡关系,且期货价格对现货价格具有显著的单向引导作用,期货市场有效发挥了价格发现功能。

可解决的实际问题:

帮助油脂油料加工企业理解期货与现货价格的内在联系,为套期保值、成本控制和风险规避提供实证依据;为投资者判断棕榈油价格走势、制定交易策略提供参考;为监管部门评估期货市场功能、完善市场机制提供数据支撑。

正文内容:

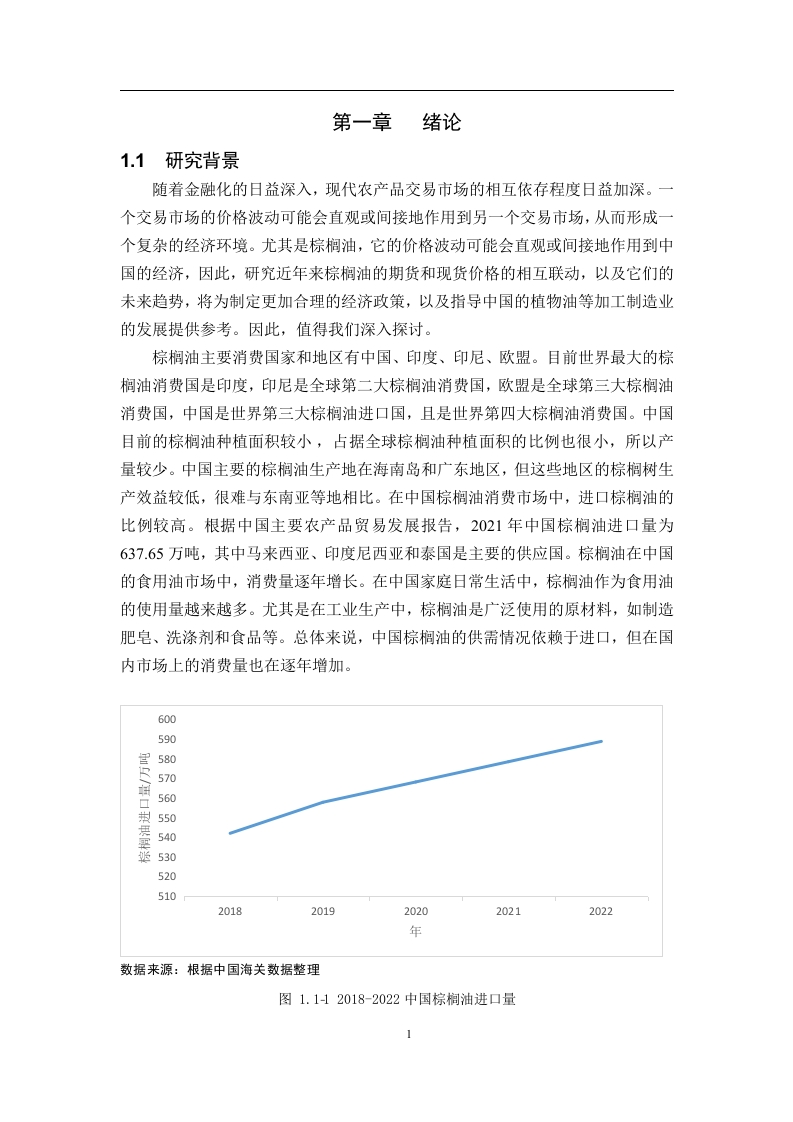

随着我国金融市场逐步完善,棕榈油作为世界主要油脂油料品种之一,在国内植物油消费中占据重要地位。因其价格低廉且难以被替代,棕榈油需求量逐年上升,对价格走势的研究有助于企业控制成本、提升利润。该研究聚焦于棕榈油期货与现货市场的价格联动关系,选取了2018年1月6日至2023年3月25日的周度数据,样本跨度超过五年,覆盖了市场波动的重要周期。

在实证方法上,论文首先通过ADF平稳性检验确认数据序列的平稳性,随后进行协整检验,结果表明国内棕榈油期现货价格之间存在长期均衡关系。格兰杰因果检验进一步揭示,棕榈油期货价格是现货价格的格兰杰原因,即期货价格单向引导现货价格,这种引导关系普遍存在。

为量化引导力度,论文构建了VAR向量自回归模型,并通过脉冲响应函数分析发现,期货价格的一个标准差冲击对现货价格产生持续且显著的影响,而现货价格对期货价格的冲击反应较弱。方差分解结果显示,期货价格对现货价格波动的解释贡献度明显高于现货对期货的解释贡献度,说明期货市场在价格发现中占据主导地位。

综合实证结果,该研究得出明确结论:国内棕榈油期货市场有效发挥了价格发现功能,期货价格能够提前反映市场信息,引导现货价格变动。这一结论对于企业利用期货工具进行风险管理具有直接指导意义。

结论与建议:

该研究通过VAR模型、协整检验、格兰杰因果检验、脉冲响应和方差分解等实证分析,系统验证了棕榈油期货价格与现货价格之间的长期均衡关系及期货价格的单向引导作用。建议油脂油料加工企业积极利用棕榈油期货进行套期保值,以锁定成本、规避价格波动风险;投资者可参考期货价格走势预判现货市场动向;监管部门应继续完善期货市场制度,提升市场透明度和有效性。

文档评价:

该论文数据选取时间跨度合理,实证方法规范严谨,结论清晰可靠,对理解中国棕榈油期现货价格联动机制具有较高参考价值。研究结果不仅丰富了期货市场功能的理论验证,也为实际产业应用提供了有力支撑。

使用建议:

适合作为学术论文的参考文献,用于期货市场与现货市场关系的研究综述或实证对比;也可作为企业培训材料,帮助从业人员理解期货价格发现功能;投资者可结合自身策略,将文中结论作为价格分析的一个辅助维度。

适用人群:油脂油料加工企业管理者、期货市场投资者、金融研究人员、高校经济类专业师生

文档核心内容:

该论文以2018年1月6日至2023年3月25日的国内棕榈油期货价格与现货价格周数据为样本,运用VAR模型、协整检验、格兰杰因果检验、脉冲响应分析和方差分解等实证方法,系统研究了中国棕榈油期货市场与现货市场之间的价格联动关系。研究证实,国内棕榈油期现货价格存在长期均衡关系,且期货价格对现货价格具有显著的单向引导作用,期货市场有效发挥了价格发现功能。

可解决的实际问题:

帮助油脂油料加工企业理解期货与现货价格的内在联系,为套期保值、成本控制和风险规避提供实证依据;为投资者判断棕榈油价格走势、制定交易策略提供参考;为监管部门评估期货市场功能、完善市场机制提供数据支撑。

正文内容:

随着我国金融市场逐步完善,棕榈油作为世界主要油脂油料品种之一,在国内植物油消费中占据重要地位。因其价格低廉且难以被替代,棕榈油需求量逐年上升,对价格走势的研究有助于企业控制成本、提升利润。该研究聚焦于棕榈油期货与现货市场的价格联动关系,选取了2018年1月6日至2023年3月25日的周度数据,样本跨度超过五年,覆盖了市场波动的重要周期。

在实证方法上,论文首先通过ADF平稳性检验确认数据序列的平稳性,随后进行协整检验,结果表明国内棕榈油期现货价格之间存在长期均衡关系。格兰杰因果检验进一步揭示,棕榈油期货价格是现货价格的格兰杰原因,即期货价格单向引导现货价格,这种引导关系普遍存在。

为量化引导力度,论文构建了VAR向量自回归模型,并通过脉冲响应函数分析发现,期货价格的一个标准差冲击对现货价格产生持续且显著的影响,而现货价格对期货价格的冲击反应较弱。方差分解结果显示,期货价格对现货价格波动的解释贡献度明显高于现货对期货的解释贡献度,说明期货市场在价格发现中占据主导地位。

综合实证结果,该研究得出明确结论:国内棕榈油期货市场有效发挥了价格发现功能,期货价格能够提前反映市场信息,引导现货价格变动。这一结论对于企业利用期货工具进行风险管理具有直接指导意义。

结论与建议:

该研究通过VAR模型、协整检验、格兰杰因果检验、脉冲响应和方差分解等实证分析,系统验证了棕榈油期货价格与现货价格之间的长期均衡关系及期货价格的单向引导作用。建议油脂油料加工企业积极利用棕榈油期货进行套期保值,以锁定成本、规避价格波动风险;投资者可参考期货价格走势预判现货市场动向;监管部门应继续完善期货市场制度,提升市场透明度和有效性。

文档评价:

该论文数据选取时间跨度合理,实证方法规范严谨,结论清晰可靠,对理解中国棕榈油期现货价格联动机制具有较高参考价值。研究结果不仅丰富了期货市场功能的理论验证,也为实际产业应用提供了有力支撑。

使用建议:

适合作为学术论文的参考文献,用于期货市场与现货市场关系的研究综述或实证对比;也可作为企业培训材料,帮助从业人员理解期货价格发现功能;投资者可结合自身策略,将文中结论作为价格分析的一个辅助维度。

第1页 / 共24页

第2页 / 共24页

第3页 / 共24页

第4页 / 共24页

第5页 / 共24页

第6页 / 共24页

第7页 / 共24页

第8页 / 共24页

试读已结束,还剩16页,您可下载完整版后进行离线阅读

付费资源

© 版权声明

文章版权归作者所有,未经允许请勿转载。

THE END

暂无评论内容