文档主要内容

文档类型:论文(本科毕业论文)

适用人群:会计学、财务管理、企业管理领域的研究者,汽车制造业财务管理人员,成本管理方向的学生及从业者

文档核心内容:

该论文以中国A股汽车制造业上市公司为样本,实证检验成本粘性的存在性及其对企业财务绩效的影响。研究基于“委托代理”“不完全契约”和“交易成本”三大理论,筛选出89家上市公司,收集2014年至2018年共248个有效数据,通过回归分析得出三项核心结论:成本粘性在汽车制造业中普遍存在;成本粘性与短期财务绩效呈显著负相关;成本粘性与长期财务绩效呈显著正相关。论文最后从内部管理优化和外部环境适应两个维度提出利用成本粘性规律提升企业绩效的对策建议。

可解决的实际问题:

帮助汽车制造企业理解成本与业务量之间的非对称变动规律,明确成本粘性对短期盈利能力和长期发展潜力的差异化影响,从而为成本控制、资源配置和战略决策提供实证依据,避免因盲目削减或保留资源而损害企业价值。

正文内容:

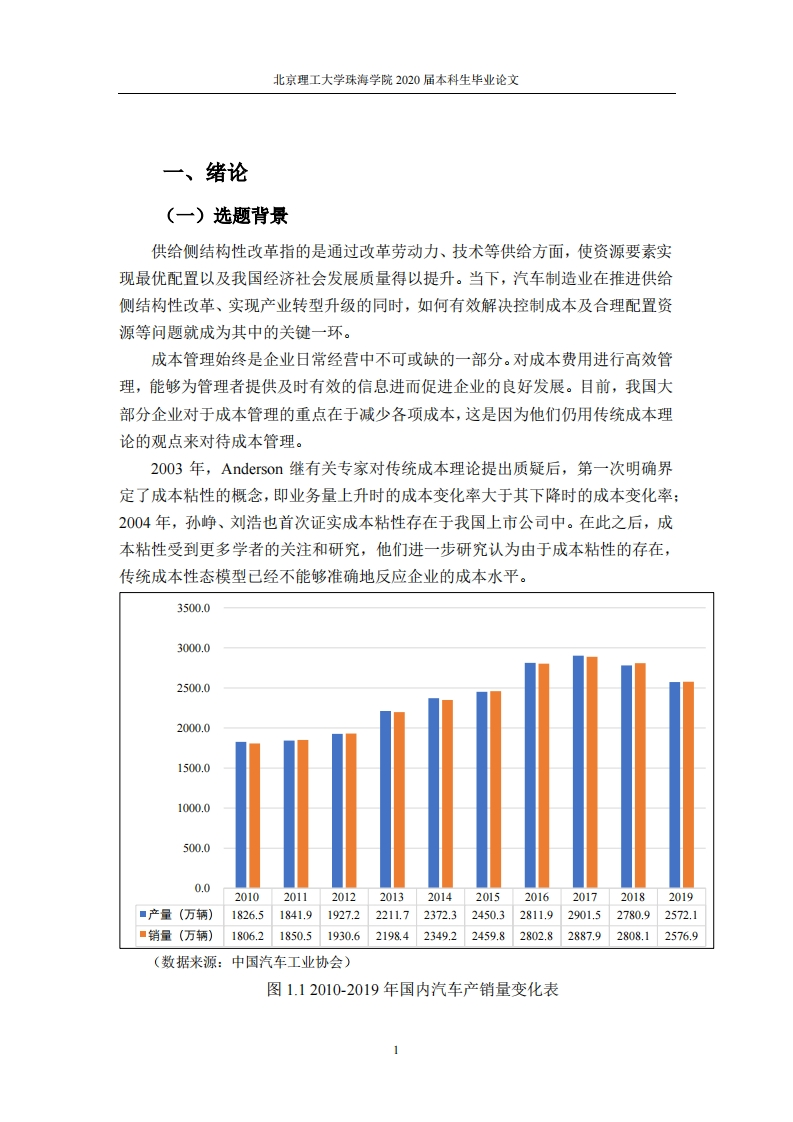

近年来,成本竞争逐渐成为企业竞争的核心,成本管理研究也随之成为会计领域的热点。大量实证研究发现,成本与业务量之间存在非对称关系:业务量上升时成本的增长幅度大于业务量下降时成本的减少幅度,这一现象被称为成本粘性。目前国内学者已证实制造业普遍存在成本粘性,但针对特定行业、尤其是汽车制造业中成本粘性对财务绩效影响的研究仍较为稀缺。

该论文选取中国A股汽车制造业上市公司作为研究对象,旨在填补这一空白。研究首先梳理了国内外相关文献,从委托代理理论、不完全契约理论和交易成本理论出发,层层筛选样本,最终确定89家上市公司,并采用2014年至2018年共248个有效数据进行实证分析。检验结果表明:中国汽车制造业上市公司确实存在成本粘性;进一步分析显示,成本粘性与企业短期财务绩效呈负相关,即成本粘性越高,短期盈利表现越差;然而,成本粘性与长期财务绩效呈正相关,说明适度保留资源有助于企业在长期获得更好的财务回报。

基于上述发现,论文从内部和外部两方面提出对策建议。内部层面,企业应优化成本管理机制,合理评估资源调整的时机与幅度,避免因过度削减成本而损害长期竞争力;外部层面,需关注行业周期与政策环境,利用成本粘性规律在业务下行期保留关键资源,为未来增长蓄力。

结论与建议:

该研究通过实证分析,首次系统揭示了A股汽车制造业上市公司成本粘性的存在性及其对财务绩效的双向影响。短期来看,成本粘性会降低当期利润,但长期而言,它有助于企业维持运营弹性、提升持续发展能力。建议汽车制造企业在制定成本策略时,区分短期绩效压力与长期战略目标,在业务收缩期审慎调整资源,避免一刀切式削减;同时加强成本动因分析,建立动态成本监控体系,使成本粘性成为企业抵御风险、实现稳健增长的有利工具。

文档评价:

该论文选题紧扣行业热点,研究方法严谨,样本选择具有代表性,结论清晰且具有实践指导意义。尤其对汽车制造业这一资本密集、成本结构复杂的行业而言,研究成果可直接应用于预算编制、产能调整和绩效评价等管理环节。不足之处在于数据时间跨度较短(仅五年),且未深入探讨不同子行业或企业规模下的差异,后续研究可进一步拓展。

使用建议:

读者可重点参考论文中的实证模型设计、变量定义及回归结果,将其作为自身研究或企业成本分析的方法论基础。汽车制造业财务人员可结合本企业实际数据,验证成本粘性水平,并依据短期与长期绩效的权衡关系优化资源分配决策。学生或研究者可借鉴其理论框架,用于其他制造业或服务业的对比研究。

暂无评论内容